Welcome to the new Traders Laboratory! Please bear with us as we finish the migration over the next few days. If you find any issues, want to leave feedback, get in touch with us, or offer suggestions please post to the Support forum here.

gojun077

-

Content Count

5 -

Joined

-

Last visited

Posts posted by gojun077

-

-

It's true that lots of limit orders are placed far away from

the current price, especially when traders are caught on the

wrong side of a move. It's kind of an attempt to 'psych' out

the market. However, it can also be a good contrary indicator,

as Steidlmayer pointed out on pg. 153 of "Steidlmayer on Markets"

(3rd Ed):

'One relevant observation I have made pertaining to watching

the book and order flow on my Trading Technologies (TT)

front end is that when the book is stacked (aggregate bids vs.

aggregate offers), the book is usually wrong. When I say

stacked, I mean it has slightly less than twice as many total

bids as total offers or slightly less than twice as many total

offers as total bids. What is probably happening is a trader or

traders on the wrong side of the market are putting in false

bids or offers defending open position, which are cancelled

once the market gets close to the trade price.'

I'm sure many of you are familiar with this situation. There might

be a huge overhang of several thousand sell orders 5 or more

ticks above the market that suddenly evaporate once aggressive

buyers start hitting the ask. I disagree that order book info is

worthless. It is certainly misleading, but that doesn't mean we

should discard it entirely. Perhaps some of you out there use the

huge imbalances (when the book is "stacked") as a clue for reversals

of intraday moves.

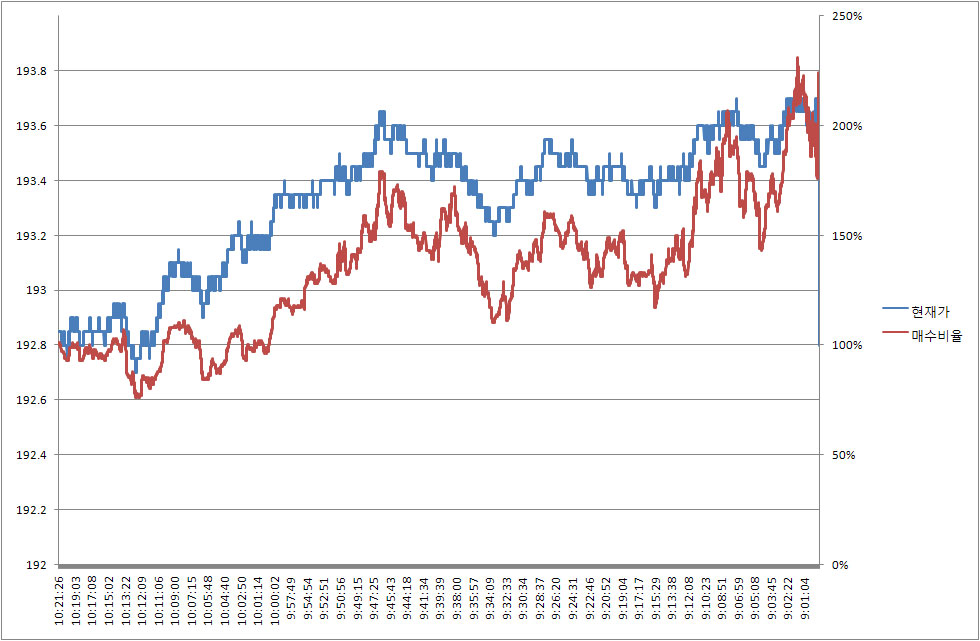

Also in S. Korea, we have an indicator called the "buy ratio" which is simply

a ratio of the outstanding buy orders to sell orders. When it's above 1,

the indicator is bullish, and when it's below 1, it's bearish. Of course,

there's more to it than just that, but really fast-moving day traders

like to use it as a momentum signal. I've attached a chart showing the

movements of the buy ratio vs. the KOSPI200 futures from April 6th. It's

pretty amazing how closely the two track each other. (the buy ratio is

in red, and the kospi200 is in blue)

-

Hi, Soultrader-

In response to your post regarding the daytrading population in S. Korea, it is

absolutely HUGE in stock index futures, namely, the KOSPI200. On some days,

individuals make up 50% of total volume! Also, options activity on ATM and

slightly OTM index options are mostly driven by retail buy-side activity. Margins are really steep, though (15% for KOSPI200 futures!), after a spate of retirees losing all their money in the futures market or getting wiped out after selling OTM naked puts.

So how is trading in Japan? I recall reading an article in the WSJ a few weeks ago that talked about housewives and salarymen currency trading after work and how individuals are getting into the yen-carry trade through futures brokerages...We're in the same time zone, apparently. It's 6:51am right now, best luck trading today!

-Jun

-

To make the OFI calculation, you would need tick data. Here in Korea,

this data is usually provided by brokerage companies free of charge

through 'HTS' (Home trading system) programs provided to customers.

The data comes in the following format:

Time Ask Bid Curr. Chg(yest) OI Theo. Fut. BASIS Volume # Sold # Bought

15:05:00 189.55 189.5 189.5 0.9 94,121 189.66 1.82 157,472 2

15:05:00 189.55 189.5 189.5 0.9 94,121 189.66 1.82 157,470 1

15:04:59 189.55 189.5 189.5 0.9 94,121 189.66 1.82 157,469 1

15:04:59 189.55 189.5 189.55 0.95 94,121 189.66 1.87 157,468 3

15:04:59 189.55 189.5 189.5 0.9 94,121 189.66 1.82 157,465 1

15:04:59 189.55 189.5 189.5 0.9 94,121 189.66 1.82 157,464 1

15:04:58 189.55 189.5 189.5 0.9 94,121 189.66 1.82 157,463 1

15:04:58 189.55 189.5 189.55 0.95 94,121 189.66 1.87 157,462 1

15:04:57 189.55 189.5 189.55 0.95 94,121 189.66 1.87 157,461 10

15:04:57 189.55 189.5 189.55 0.95 94,121 189.66 1.87 157,451 1

15:04:57 189.55 189.5 189.55 0.95 94,121 189.66 1.87 157,450 5

15:04:56 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,445 1

15:04:56 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,444 1

15:04:56 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,443 2

15:04:56 189.55 189.5 189.5 0.9 94,109 189.66 1.82 157,441 6

15:04:55 189.55 189.5 189.5 0.9 94,109 189.66 1.82 157,435 5

15:04:54 189.55 189.5 189.5 0.9 94,109 189.66 1.82 157,430 5

15:04:53 189.55 189.5 189.5 0.9 94,109 189.66 1.82 157,425 1

15:04:53 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,424 3

15:04:51 189.55 189.5 189.5 0.9 94,109 189.66 1.82 157,421 5

15:04:50 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,416 2

15:04:49 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,414 2

15:04:49 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,412 15

15:04:49 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,397 1

15:04:49 189.55 189.5 189.5 0.9 94,109 189.66 1.82 157,396 7

15:04:49 189.55 189.5 189.55 0.95 94,109 189.66 1.87 157,389 1

(I apologize for the poor formatting- it looks nice on my screen, but the exported text is hard to read) I'm sure similar data is available from your service providers' screens. Once you have the tick data, simply calculate the average of the contracts sold column, and do the same for the contracts bought column. Then divide (avg bought)/(avg sold)

and you get your OFI. As I stated in my earlier post, there are different ways to calculate OFI. This is the easiest method.

The second method requires data from the limit order book. It takes into account the number and size of orders in the order book in calculating OFI.

First, the formula:

(Total # of contracts bot/# of buy side contracts in order book) / (Total # of contracts sold/# sell side contracts in order book)

Sometimes, however, I feel the second method gives a misleadingly low OFI figure. Consider the case of a monster up day. On such a day, there will be a large bias of longs vs shorts. When we divide the number of Total contracts bought by the huge number of unfilled orders in the order book, the numerator of the OFI will be small. Let me illustrate with some real numbers from the KOSPI200 futures on 3-27:

75,047 contracts sold, 84,676 contracts bought

avg number of contracts on the sell side of the limit order book: 3,781

avg number of contracts on the buy side of the limit order book: 5,658

(84,676/5,658) / (75,047/3,781) = 0.75, a very bearish OFI figure, but using the first method above, we get:

avg size of buys: 6.76 contracts, avg size of sells: 6.07 contracts,

OFI = 6.76/6.07 = 1.11, a moderately bullish OFI figure

Although MP is getting quite popular among day traders here in S. Korea, the OFI concept is still not well-known. I'm still in the process of gathering data for OFI correlation to the next morning's up/down movement. I will post my findings after gathering a few weeks' data...

-

In "Steidlmayer On Markets" 2nd edition (2003), Steidlmayer talks about

OFI (On-Floor Information) as an indicator for trading the first three time

periods for the following day. If OFI for the previous day is <1.0, then we

should consider going short the next morning, and if OFI > 1.0, long.

The formula for calculating OFI was simply:

OFI = AVG SIZE OF FILLED BUY ORDERS/AVG SIZE OF FILLED SELL ORDERS

However, in an interview with Active Trader Magazine in the September 2005

issue, the formula for On-Floor Information was a bit different:

OFI= (Bought contracts/buy orders) / (Sold Contracts/Sell Orders)

The resulting OFI figures can be quite different when we factor in the number

of contracts entered in the limit order book

(the divisor in the second formula above).

In my casual empirical observation of OFI figures and the next morning's move

in KOSPI200 futures, OFI doesn't seem to be a good predictor in this

market.

My question is- does anyone else use OFI in their trading, and which method

do you use to calculate the OFI figure?

Cheers from South Korea,

Jun

(I apologize for starting a new thread as a newbie...)

MP on excel

in Market Profile

Posted

Kudos to bobajob on a great MP spreadsheet. It was just brilliant of you

to think of using CONCATENATE to create the row of letters from the separate letter columns! I have made a small addition to your

spreadsheet "ES Profile Maker Next Gen."

I added a feature that will calculate volume per tick using tick data for

the KOSPI200. In bobajob's current implementation, the profile appears

perfectly, but there is no volume information for how many contracts

were traded at each price point. I hope everyone will find this minor

addition useful. This feature was added using the excel function SUMIF.

Cheers,

Jun

MP2-26-07 example.rar